One of the most important considerations in China's industrial and technical development has always been the principle of not allowing important strategic goods or materials to fall under the control of other nations. Although China currently relies on imports for the vast majority of 32-inch or larger LCD TV panels, with the country's role largely limited to LCM assembly, China's policy guidelines for the development of the flat panel display industry signal that the country intends to fill in the gaps in its existing supply chains.

This includes upstream components and materials, as well as LCD panels, and the scale of state subsidies to homegrown panel manufacturers such as BOE and China Star Optoelectronics demonstrates the government's commitment to this endeavor. TFT LCDs also have enormous output value, making them of considerable use in efforts to boost local economies and GDP figures. For this reason, a wave of enthusiasm for building advanced production lines has swept through China over the last year or two.

In addition, China's low labor costs and abundant workforce, combined with the continuing improvements in its production supply chain efficiency, have led almost 95% of Taiwan-based electronics manufacturers to locate their overseas production sites principally in China. Driven by the two key factors of production and local demand, China is fast becoming the location of choice for manufacturers wishing to set up new TFT LCD production lines.

The combination of sustained growth in China's domestic demand and its growing exports of LCD products in downstream applications, means China is set to become a new challenge that global display panel manufacturers cannot afford to ignore over the next 2-3 years.

The DIGITIMES Research Special Report, "China TFT LCD panel industry overview," provides and in-depth examination of China's TFT LCD sector, including analysis of the proactive policies China uses to support its flat panel display industry, forecasts of local and global large-size LCD demand and the expected development of the local TFT LCD supply chain, as well as providing multiple large-size TFT LCD production line capacity scenarios for the Greater China region over the next few years.

Chart 1: Why China is developing advanced LCD production lines

Table 1: Overview of plans for 7.5G+ production lines in China

Chart 3: China's share of system production of major LCD panel applications, 2008-2010

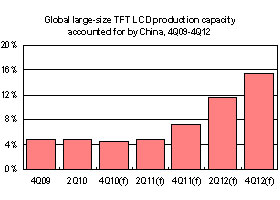

Chart 4: Global large-size TFT LCD production capacity accounted for by China and Japan, 4Q09-4Q12

China proactive policies to support flat panel display industry

Chart 5: China policy directives regarding display panel industry development

Support for local panel manufacturers through tax incentives and subsidies

Chart 8: Government assistance to BOE Technology Group, 2008-2009 (Total of CNY760 million)

Chart 11: LCD monitor shipments in China, 2008-2013 (m units)

Production volume analyses for large TFT LCD panels in China

Chart 12: Production and annual growth rates for key electronic products in China, 2009 (k units)

Chart 14: Production volumes and global share of LCD TVs manufactured in China, 2008-2013 (k units)

Large-size TFT LCD production lines in Greater China and capacity scenarios

Taiwan-based manufacturers' large TFT LCD production line capacity and development plans

Table 2: Overview of Taiwan-based manufacturers' 6G or higher generation TFT LCD production lines

China-based manufacturers' large TFT LCD production line capacity and development plans

Capacity development scenarios for large TFT LCD production lines in China

BOE receiving the most proactive support from government policy

Chart 28: Beijing Municipal Government is actually BOE's largest shareholder

Chart 29: BOE revenues and post-tax net profits, 2004-2010 (CNYm)

Chart 32: BOE large-size TFT LCD production capacity, 1Q10-4Q12 (k square meters/quarter)

Table 7: China Star Optoelectronics' 8.5G fab expected to begin mass production in 4Q11

Chart 33: BOE's 8.5G production line is further along schedule that that of CSOT

Chart 34: TCL LCD TV sales between January and September 2010 were less than ideal (k units)

Chart 35: TCL Corporation's revenue and profit results over recent quarters (CNYm)

Development of the component supply chain for BOE's advanced production lines

Chart 37: Component supply chain for CSOT (Shenzhen) 8.5G fab

Chart 38: Shenzhen Textile Holdings turnover and net profits, 2008-3Q10 (CNYm)

Chart 41: AUO has strengthened its close relationships with customers through joint investments

Taiwan-based manufacturers' China fab strategies and operational analysis

Chart 42: Competitive advantages for China-based TFT LCD panel manufacturers

Chart 44: Shenzhen Municipal Government hopes to induce AUO or Samsung Electronics to invest in CSOT

Development of advanced fabs in China by Chimei Innolux (CMI)

Table 8: Development of Chengdu High-tech Industrial Development Zone (CDHT)