For major application processor manufacturers, 2012 is a year fraught with far more intense competition and challenges than any previous year. This is largely due to increased consumer performance requirements for mobile devices, the rapid increase in users in emerging markets, and the accelerating pace of development in terms of technology, architectures and price competition. Over the last year alone, greater advances in manufacturing processes and performance improvements for ARM architecture-based application processors (AP) have been made than in the last few years combined.

China-based manufacturers will catch up with mainstream AP architectures in the second half of 2012, with Cortex-A9 becoming the mainstream, augmented by a smaller proportion of chips using Cortex-A7 and Cortex-A5, while Cortex-A8 will gradually exit the market. In the fourth quarter, some China manufacturers will begin to ship quad-core products for use in smartphones and tablets.

Digitimes Research calculates that nearly 300 million smart devices (smartphones and tablets) will be shipped in China in 2012, with smartphones accounting for some 240 million of this figure, and tablets for the remainder. This represents growth of three to four times over the 2011 figures. However, the China market is entering a period of intense price reductions with many vendors launching sub-CNY199 smartphones; this could have an unhealthy impact on the market, even to the extent of hastening the demise of some manufacturers.

Chart 1: Platform roadmap for mainstream white-box tablets in China, 2012-2013

Chart 3: China smart device market seeing massive growth in 2012 (m units)

Competition and collaboration for different telecom standards

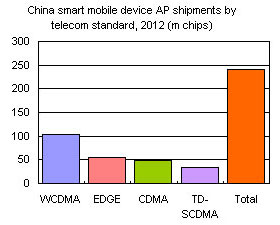

Chart 4: China smart mobile device AP shipments by telecom standard, 2012 (m chips)

Chart 5: China mainstream smartphone platform development roadmap

Chart 6: AllWinner's 2H12 product line creates a vacuum for competitors

Chart 7: AllWinner price/performance ratio ratio will be lacking in 4Q12

Chart 8: Smartphone cost and device price trends in the China market (CNY)

Chart 9: Usage trends for China smartphone core architectures

Chart 10: China smartphone shipment share by telecom standard

Chart 12: China market TD-SCDMA smartphone chip shipments, 2012 (m chips)

Chart 14: MediaTek quarterly smartphone chip shipment share by product, 2012

Chart 15: MediaTek smartphone chipset price trends, 2012 (US$)

Chart 16: Qualcomm chip products for the China smartphone market, 2012-2013

Chart 17: Qualcomm quarterly China smartphone chips shipment share by product, 2012

Chart 18: Price trends for Qualcomm's China smartphone chipsets, 2012 (US$)

Chart 19: Spreadtrum smartphone chip product roadmap, 2012-2013

Chart 20: Spreadtrum quarterly smartphone chip shipment share by product, 2012

Chart 21: Price trends for Spreadtrum's smartphone chipsets, 2012 (US$)

Chart 22: China market share of major smartphone chip manufacturers in 2012 (m chips)

Table 2: Quarterly China shipments for major smartphone chip makers, 2012 (k chips)

Chart 23: China tablet chip shipments by domestic supplier, 2012 (m chips)

Chart 24: Cortex-A9 becomes mainstream architecture for midrange and high-end tablets

Chart 25: MIPS-based processors now have just 3.7% of the China tablet AP market

Chart 28: TI tablet chip shipments by quarter in China, 2012 (m chips)

Chart 29: Path Nvidia takes will be determined by changes in the discrete GPU market

Table 3: Quarterly China shipments for major tablet chip makers, 2012 (m chips)

Table 4: Q3 list prices for the main tablet chip products in 2012