During the 10th and 11th Five Year Plan (FYP) periods from 2001-2010, the China's government listed the semiconductor industry as one of the key industries to be supported.

Spurred on by State Council Rule 18 (2000), major China-based foundry firms such as SMIC, Hejian, Grace, and TSMC's Songjiang operations were founded during the 10th FYP period and began to rapidly expand capacity. The result was that output value for China's merchant foundry industry grew from CNY3.6 billion in 2001 to CNY22.1 billion in 2010, representing an annual compound growth rate of 21%. With this, China's IC manufacturing firms truly took off and entered a period of growth.

While the output value of China's semiconductor industry grew significantly during the 10th and 11th FYP periods, the industry's overall level of competitiveness remained weak. During the 12th FYP period from 2011-2015, China's semiconductor industry policy will shift the emphasis for development away from the pursuit of capacity and output value growth, towards a focus on improving R&D capabilities for advanced technology and advanced capacity. The government's earlier method of pouring funds directly into the industry will also be replaced by an emphasis on strengthening the operations of market mechanisms, in order to foster a group of semiconductor firms with global market share and the capacity for technological innovation.

China's policies on semiconductor development during the 12th FYP period include the Outline of the 12th Five Year Plan for National Economic and Social Development, State Council Rule 32 (2010), the six major measures to develop the software and semiconductor industries, and State Council Rule 4 (2011).

Besides affirming the semiconductor industry as one link in efforts to build infrastructure for next generation IT within the strategy for seven new major strategic industries, these plans also confirmed that semiconductor firms that met the appropriate conditions would be eligible to receive government support; moreover, the government would work to strengthen the industry's capacity for independent technological innovation through a raft of measures to reform tax incentive policy, as well as to improve the function of financial markets.

This report also provides forecasts and analysis regarding the prospects for merchant foundry firms such as SMIC, Huahong NEC, Grace, Huali Microelectronics (HLMC), Jiangsu Changjiang (JCET), Nantong Fujitsu Microelectronics (NFME), Spreadtrum and HiSense, as well as for leading package testing and IC design firms, during the 12th FYP period.

The report concludes with projections and analyses on the prospects for the IC manufacturing and IC design industries in China under the influence of the new semiconductor industry polices of the 12th FYP during the 2011-2015 period.

Evolution of China's semiconductor industry leading up to 12th Five Year Plan

Development of the China semiconductor industry prior to the 10th Five Year Plan

Chart 1: Policy direction and objectives in the 10th and 11th FYPs

Chart 2: Policy to support semiconductor industry development in the 10th and 11th FYPs

Chart 3: Chinese government subsidies to SMIC, 2002-2009 (US$k)

Development of China's semiconductor industry during the 10th and 11th FYPs

Chart 4: Output value of China IC design industry, 2001-2010 (CNYm)

Chart 7: Initial establishment of merchant foundries in China, by company

Chart 8: Capacity for China's major merchant foundry firms, 1992-2011

Table 1: China-based merchant foundry firms' monthly capacity and process technologies, 4Q10

Chart 9: Technological progress comparison between TSMC, UMC, SMIC and Grace, 2003-2010

China semiconductor assembly and testing services (SATS) industry

Chart 10: NFME and CJET's revenues and share of China SATS industry output value, 2006-2010 (CNYm)

Chart 11: R&D progress and future plans for China's major specialist SATS firms, 2000-2010

Chart 13: Output value for the China IC design industry, 2006-2010 (CNYb)

Chart 14: IC design share of China IC industry output value, 2006-2010

Chart 15: China share of global IC design industry output value, 2006-2010

Status of China's semiconductor industry after the 11th FYP period

Chart 16: China merchant foundry industry output value, 2001-2010 (CNYm)

Chart 17: China SATS industry output value, 2001-2010 (CNYb)

Chart 18: China semiconductor industry output value, 2001-2010 (CNYm)

Chart 21: Distribution of output value and companies in semiconductor industry clusters

Chart 22: Status of semiconductor industry clusters in the Bohai Rim region

Chart 23: Status of semiconductor industry clusters in the Yangtze River Delta region

Chart 24: Status of semiconductor industry clusters in the Pearl River Delta region

Chart 25: Status of semiconductor industry clusters in the Western Triangle region

Provisions of the 12th FYP and associated policies affecting the semiconductor industry

Chart 27: Seven major strategic new industries in State Council Rule 32 (2010)

Chart 28: Policies to support the seven strategic new industries in State Council Rule 32 (2010)

Chart 31: SMIC revenues and share of total China revenues, 2007-2010

Chart 32: Policy directions to support the semiconductor industry in the 12th FYP

State Council's six major measures to develop the software and semiconductor industries

Analysis of 12th FYP policies on the IC manufacturing industry

Increasing and accelerating the concentration of the industry

Continuing to increase the number of firms through fundraising from securities market listings

Chart 39: Financing/fundraising policy for IC design firms in State Council Rule 32 (2010)

Trend 2: The degree of concentration among IC design firms continues to increase;

Chart 42: State Council Rule 4 (2011) - Policy objectives to support the IC design industry

Chart 43: State Council Rule 4 (2011) - Tax incentives for IC design firms

Chart 45: State Council Rule 32 (2010): Key areas of next generation IT

Chart 46: China IC design firms' current activities in the mobile sector

Chart 47: Branded products using IC solutions from China-based IC design firms

Chart 48: SMIC 8-inch and 12-inch wafer capacity, 2Q08-1Q11 (8-inch equivalent Kpcs)

Chart 49: SMIC revenue breakdown by geographic region, 2002-2010 (m US$)

Chart 50: SMIC revenue share by manufacturing process, 1Q09-1Q11

Chart 52: Changes in SMIC's equity structure, 2004-2011 (m shares/%)

Chart 53: Government policy support and targets for SMIC during the 10th to 12th FYP periods

Chart 54: Technology roadmap for Grace, Hua Hong NEC and HLMC, 1Q11-4Q12

Jiangsu Changjiang Electronics Technology (JCET) and Nantong Fujitsu Microelectronics (NFME)

Chart 57: Revenues and EPS for JCET and NFME, 2005-2010 (CNYm/CNY)

Chart 58: Subsidies for SATS firms and associated equipment manufacturers in China's Project 02

Table 5: 2010 rankings of China's Top 10 IC design firms (CNYb)

Chart 59: Product launch schedules for baseband IC firms in the Greater China region, 2009-2011

China semiconductor industry forecast during the 12th FYP period

Trend 1: The concentration of the merchant foundry industry continues to increase

Chart 62: China-based merchant foundry quarterly capacity, 2010-2015 (k units 8-inch equivalent)

Trend 2: China's government will continue to increase its stake in the leading foundry firms

Chart 65: Output value for China's SATS and merchant foundry industries, 2005-2015 (CNYb)

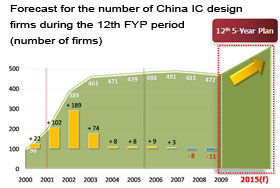

Outlook for the China IC design industry during the 12th FYP period

Chart 67: China IC design industry output value during the 12th FYP period (CNYb)

IC design as a share of overall output value for the China IC industry