Global sales of total semiconductor manufacturing equipment by original equipment manufacturers are forecast to set a new industry record, reaching $109 billion in 2024, growing 3.4% year-on-year, SEMI announced today in its Mid-Year Total Semiconductor Equipment Forecast – OEM Perspective at SEMICON West 2024. Semiconductor manufacturing equipment growth is expected to continue in 2025, with sales forecast to set a new high of $128 billion in 2025, driven by both the front-end and back-end segments.

"The growth in total semiconductor manufacturing equipment sales already underway this year is forecast to be followed by a robust expansion of roughly 17% in 2025," said Ajit Manocha, SEMI president and CEO. "The global semiconductor industry is demonstrating its strong fundamentals and growth potential supporting the diverse range of disruptive applications emerging from the Artificial Intelligence wave."

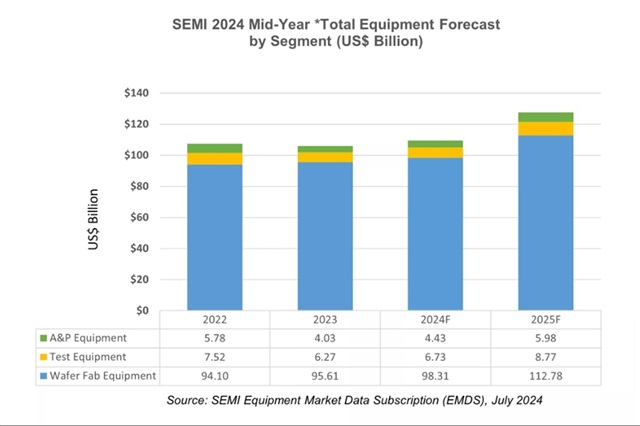

Semiconductor Equipment Sales by Segment

After registering a record $96 billion in sales last year, the wafer fab equipment segment, which includes wafer processing, fab facilities, and mask/reticle equipment, is projected to increase by 2.8% to $98 billion in 2024. This marks a notable increase from the previously forecasted $93 billion in SEMI's 2023 Year-End Equipment Forecast.

Ongoing strong equipment spending in China and substantial investments in DRAM and HBM, driven by AI computing, drove the upward revision. Looking ahead to 2025, Wafer fab equipment segment sales are projected to expand by 14.7%, reaching $113 billion due to increased demand for advanced logic and memory applications.

Following two years of contraction caused by challenging macroeconomic conditions and softening semiconductor demand, the back-end equipment segment is anticipated to start its recovery in the second half of 2024. Specifically, sales of semiconductor test equipment are projected to rise 7.4% to $6.7 billion in 2024, while assembly and packaging equipment sales are predicted to increase 10.0% to $4.4 billion in the same year.

Furthermore, back-end segment growth is expected to accelerate in 2025, with test equipment sales surging 30.3% and assembly and packaging sales increasing 34.9%. The segment's growth is supported by the increasing complexity of semiconductor devices for high-performance computing and the expected recovery in demand for automotive, industrial, and consumer electronics end-markets. Additionally, back-end growth is expected to increase over time to process ramping supply from new front-end fabs.

*Total equipment includes new wafer fab, test, assembly and packaging. Total equipment excludes wafer manufacturing equipment. Totals may not add up due to rounding.

Wafer Fab Equipment (WFE) Sales by Application

Wafer Fab Equipment sales for foundry and logic applications are expected to show a moderate contraction of 2.9% year-over-year to $57.2 billion in 2024 due to a softening in demand for mature nodes and higher-than-expected sales for advanced nodes in the previous year. The segment is forecast to grow 10.3% in 2025 to $63.0 billion, driven by increasing demand for leading-edge technology, the introduction of new device architectures, and increased capacity expansion purchases.

Memory-related capital expenditures are projected to see the most significant increase in 2024 and demonstrate continued growth in 2025. NAND equipment sales are expected to remain relatively stable in 2024, with a 1.5% increase to $9.35 billion, as supply and demand normalize, setting the stage for a 55.5% expansion to $14.6 billion in 2025. Meanwhile, DRAM equipment sales are projected to grow strongly at 24.1% and 12.3% in 2024 and 2025, respectively, supported by surging demand for High-Bandwidth Memory (HBM) for AI deployment and ongoing technology migration.

Semiconductor Equipment Sales by Region

China, Taiwan, and South Korea are expected to remain the top three destinations for equipment spending through 2025. China is projected to maintain the top position over the forecast period as the region's equipment purchases continue to rise.

Equipment shipments to China are projected to exceed a record $35 billion in 2024, solidifying its lead over other regions. While equipment spending for some regions is expected to fall in 2024 before rebounding in 2025, China is expected to see a contraction in 2025 following significant investments over the past three years.

The SEMI forecast is based on collective input from top equipment suppliers, the SEMI Worldwide Semiconductor Equipment Market Statistics (WWSEMS) data collection program, and the industry-recognized SEMI World Fab Forecast database.

Credit: Semi