Analysts gave Alibaba Group Holding's latest results a cautious reception, warning that surging artificial intelligence (AI) investments are pressuring profitability even as cloud growth accelerates. While investors welcomed strong AI-related momentum and rising cloud revenue, several research firms said heavy infrastructure spending and weaker-than-expected earnings underscored the mounting costs of Alibaba's ambitious AI expansion.

Alibaba Group management signaled a fundamental shift in its business model during the fourth-quarter fiscal year 2026 earnings call, held on May 13, transitioning from a traditional e-commerce and cloud provider into an "AI-first" ecosystem. CEO Eddie Wu described the company as being at a "pivotal inflection point," moving beyond initial experiments with conversational chatbots toward the deployment of autonomous AI agents. A robust balance sheet and a massive expansion of physical data center infrastructure back this strategic pivot.

Group financial performance and shareholder returns

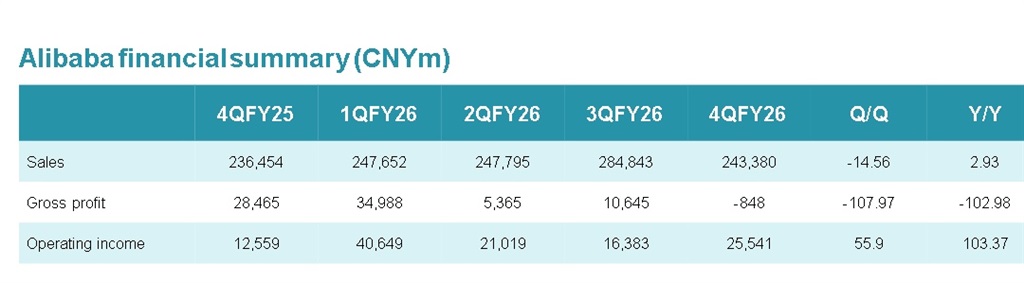

Alibaba reported consolidated revenue of CNY243.4 billion (approx. US$35.84 billion) for the quarter, an 11% year-over-year increase. While GAAP net income rose 96% to CNY23.5 billion, adjusted EBITDA fell 84% to CNY4.5 billion, primarily due to "high intensity investment" in AI technology and user experience improvements.

The company maintains a formidable liquidity position with approximately US$59 billion in net cash, excluding long-term debt. Consequently, the board approved an annual dividend of US$1.05 per ADS, reinforcing management's commitment to consistent shareholder returns despite heavy capital outlays.

The rise of autonomous agents and the Qwen ecosystem

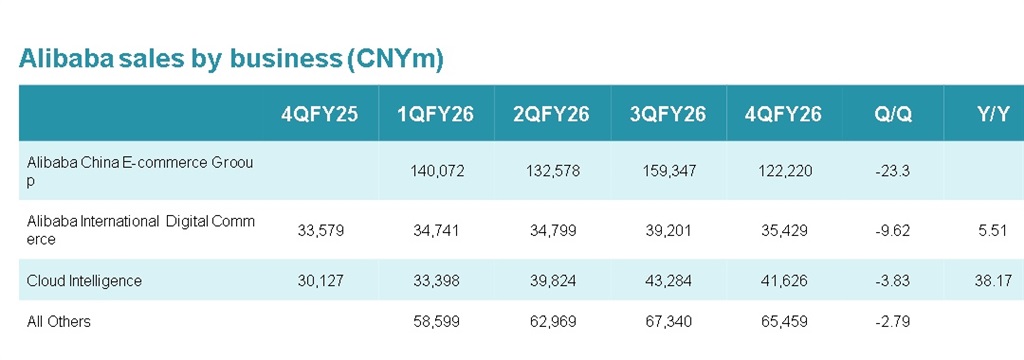

A central theme of the call was the rapid commercialization of Alibaba's AI software stack. Management highlighted that the Cloud Intelligence Group's external revenue growth accelerated to 40%, driven by AI-related products that have maintained triple-digit growth for 11 consecutive quarters. AI-related revenue now accounts for 30% of external cloud revenue, a figure management expects will "cross the 50% threshold" within the next year as it becomes the primary engine for growth.

Alibaba is heavily promoting its "Model-as-a-Service" (MaaS) platform, known as Model Studio. This platform serves as an open environment for both Alibaba's proprietary models, such as the Qwen (QN) series, and various third-party models. CEO Eddie Wu revealed that the annualized recurring revenue (ARR) for model and application services has already surpassed CNY8 billion, an increase of more than 10 times since late 2025. Management expects this ARR to "surpass CNY10 billion in the June quarter and CNY30 billion by year-end".

The evolution of the "Qwen ecosystem" was further solidified on May 7th, when the QN app fully integrated the commerce and service capabilities of Taobao, Tmall, Alipay, Amap, and Fliggy. This integration has positioned the QN app as China's "first all-in-one personal assistant" designed to bridge productivity, learning, and daily life. On the enterprise side, management noted that AI coding has emerged as one of the fastest-growing sectors.

Wu stated that these models are not merely replacing engineers but are "able to solve a wide array of very complex tasks" across any digitalized workplace scenario. Management believes that as these models provide "truly valuable intelligence," the historical reluctance of Chinese customers to pay for software-as-a-service (SaaS) will diminish.

Scaling the AI hardware moat and infrastructure investments

To support the "explosive growth" in training, inference, and agent orchestration, Alibaba is aggressively expanding its physical footprint. Management compared its current investment strategy to building "factories," specifically an "AI training factory" and an "inferencing factory" powered by massive data centers. To meet projected demand, Alibaba anticipates needing "10 times the amount of data center infrastructure" by 2033 compared to its 2022 levels.

This massive expansion is expected to drive spending beyond the company's previously stated five-year capex target. "It's likely... that we will overshoot the original Capex figure that we had stated of CNY380 billion," management noted. This spending comes amid a challenging global environment for hardware; the company reported that the "cost for us to deploy one new server this year is double what that same server would have cost a year ago," representing a 100% inflation in replacement costs.

Alibaba views its self-developed hardware as a critical "durable moat" against these rising costs and supply chain uncertainties. The company's T-Head proprietary GPU chips have achieved "scaled mass production," with over 60% of that compute capacity already serving external customers across sectors such as financial services and autonomous driving. As the only cloud provider in China capable of delivering self-developed AI chips at scale, Alibaba claims it has secured "autonomy over our compute supply-chain".

CFO Toby Xu addressed concerns regarding negative free cash flow during the quarter, attributing it directly to these "very significant investments". He emphasized that management remains "extremely resolute" in this spending, viewing the next two years as a "critical window of opportunity".

Management expressed confidence that these investments will eventually lead to higher net cash flow as AI offerings command higher gross margins than traditional cloud compute and storage services. Wu concluded that today "there isn't a single card on our servers that is idle," indicating that the immediate return on investment for new infrastructure remains high.

AI investment costs weigh on margins despite solid cloud growth momentum

Alibaba Group's latest quarterly results drew a mixed response from analysts, with some warning that aggressive AI spending is weighing on profitability despite strong cloud growth.

According to Bloomberg Intelligence, Alibaba's weak fiscal 2026 results reinforced concerns that AI investments may continue to hurt returns at China's leading AI firms. The research house said the company remained "burdened by the heavy cost of AI-related investments."

Analysts at Citi, which maintains a buy rating and a US$205 price target on Alibaba, said the results were mixed, with both revenue and profit missing expectations. Citi noted that external cloud revenue rose 40% year over year, while total cloud revenue increased 38%, below its own and consensus forecasts of 41% and 40%, respectively.

Vital Knowledge also described the overall earnings as "pretty underwhelming," although it said investors would likely welcome Alibaba's cloud performance and AI-related momentum.

Credit: Alibaba, May 2026

Credit: Alibaba, May 2026

Article edited by Jack Wu